OVERVIEW

FINANCING NEEDS AND OPPORTUNITIES

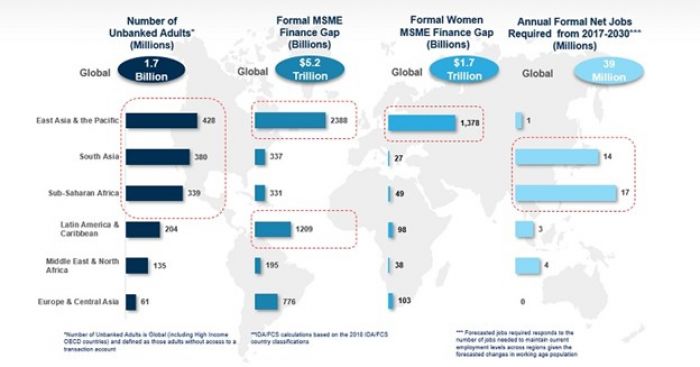

SMEs are less likely than big businesses to be able to get a banking loan. They, therefore, rely on domestic funding or funds from friends or relatives to start and initially operate their businesses. The International Finance Corporate (IFC) reports that there’s an unmet funding need of $5.2 billion per annum, equal to 1,4 times the current amount of the global MSME lending is presented by 65 million companies, or 40% of formally-owned micro, small and medium-sized enterprises (MSME). The highest share (46%) of the global financial gap in East Asia & the Pacific is followed by Latin America & the Caribbean (23%) and Europe & Central Asia (15%). Approximately half of formal SMEs have no formal borrowing available. If micro and informal companies are considered, the funding deficit is much greater.

SME INVESTMENT CONCEPT

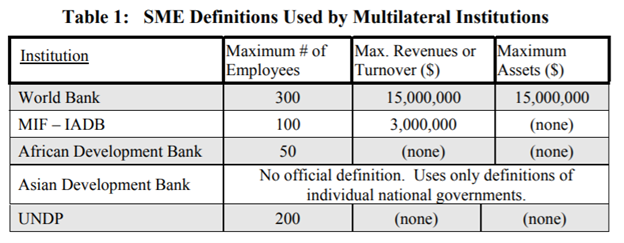

The room between micro and big companies is mostly occupied by small and medium-sized businesses (SMEs). Definitions of what constitutes an SME are often undefined and differ widely between markets, governments, and financial institutions. The criteria most often adopted are the number of employees or the annual revenue of a company; (turnover). The firms in which most of our SME investors invest are mostly employing between 20 and 250 employees in these traditional groups and have an annual income of between $200,000 and $15 million. Although the amounts vary considerably for different investment funds, sectors of business, and regions.

THE MISSING CORE

So far, we’ve established that SMEs are important to every nation’s health and stability. They constitute historically the largest share of the job base, recruit the newest workers, and provide most goods and services in a country. A thriving small business market and an increasing middle-income community are lacking in many developing countries. Yet despite their significance, small and medium-sized enterprises in emerging markets are often not given adequate access to finance preventing their expansion and their ability to make a major social and economic influence. Entrepreneurs looking for funding in such markets are against local commercial banks’ view that small and medium-sized businesses are too ‘risky’ for conventional loans and yet too big for the increasing range of microfinance programmes. This funding gap leads to what is more and more known as the missing core.

In our experience, the lack of risk resources in the absent medium significantly reduces these small and medium-sized enterprises’ capacity for growth and, therefore, has a profoundly negative effect in terms of wages, middle-class development, and fiscal revenues, which are critical for a country’s social sector development. A thriving middle economy is a core component of employment creation, job training, elimination of poverty, wealth development, sustained economic growth, and prosperity.

THE OPPORTUNITIES

Through our experience, we’ve known that sustainable economic growth is driven by direct investment in SMEs. We have seen first-hand that promoting growth by providing access to risk capital and business support for such companies will encourage the enterprise, while accelerating development in its surroundings, to resolve its impediment to growth and to produce higher value-added goods or services for both domestic and foreign consumers. SME investment leverages promising enterprises in local communities and markets to catalyze socio-economic development and entrepreneurship. Such investment also generates significant returns for our investors if realised correctly and sustainably.

{kind=link}